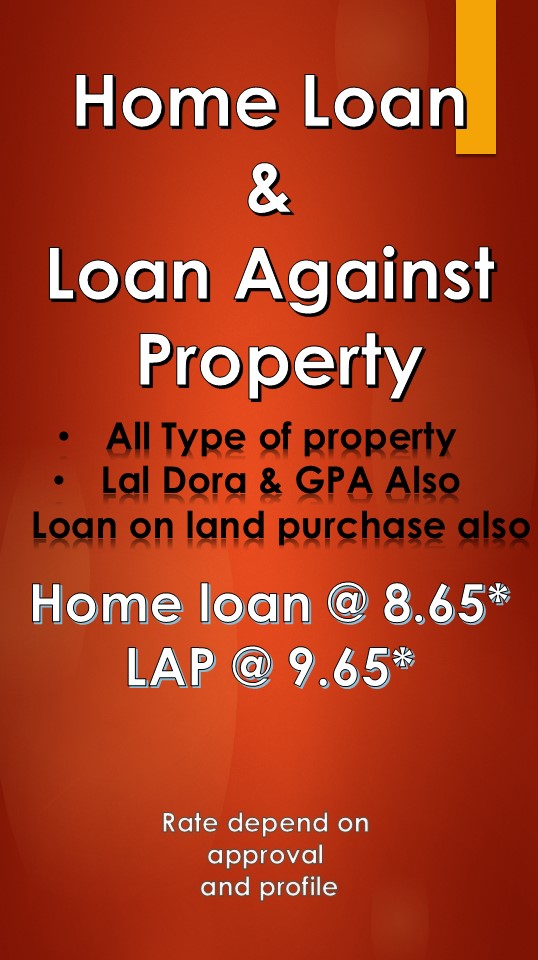

Understanding Loan Against Property (LAP)

A loan against property (LAP) is a secured loan where borrowers pledge their residential, commercial, or industrial property as collateral to avail a loan from a bank or financial institution. This form of loan is advantageous for both lenders and borrowers, providing a mutually beneficial financial solution.

How Does Loan Against Property Work?

The mechanism of LAP is straightforward. Here’s a step-by-step outline:

Property Valuation: The first step involves the valuation of the property to be mortgaged. Banks or financial institutions typically conduct this process through their approved evaluators.

Loan Application: After the valuation, the borrower submits a loan application. This application includes personal details, income proof, property documents, and other necessary financial information.

Loan Approval: Based on the property's value and the borrower’s creditworthiness, the lender approves a loan amount. Typically, lenders sanction around 50-70% of the property's current market value.

Disbursement: Upon approval, the loan amount is disbursed to the borrower, which can be used for various purposes such as business expansion, debt consolidation, education, medical expenses, or any other financial requirement.

Repayment: The borrower repays the loan through equated monthly installments (EMIs) over a specified tenure, which can range from 5 to 20 years or more. The interest rate is generally lower compared to unsecured loans due to the collateral involved.

Features of Loan Against Property

High Loan Amount: Since LAP is a secured loan, lenders offer a significant loan amount, which can range from thousands to millions, depending on the property's value and the borrower’s repayment capacity.

Lower Interest Rates: The interest rates on LAP are comparatively lower than unsecured loans like personal loans. This is due to the reduced risk for lenders, as the property acts as collateral.

Flexible Tenure: Borrowers can choose a tenure that suits their financial situation, making the repayment process manageable. Longer tenures mean smaller EMIs, though the total interest paid over the loan period will be higher.

Multipurpose Use: The funds obtained through LAP can be used for any legitimate financial need, offering great flexibility to the borrower.

Retention of Ownership: Even though the property is mortgaged, the borrower retains ownership and can continue using it. The property only changes hands if the borrower defaults on loan repayment.

Advantages of Loan Against Property

Lower Interest Rates: As mentioned, one of the primary advantages is the lower interest rates compared to unsecured loans, making LAP a cost-effective borrowing option.

Long Repayment Tenure: With the possibility of extending the loan tenure up to 20 years or more, borrowers can manage their finances more comfortably with affordable EMIs.

Large Loan Amount: The higher loan amounts available under LAP can help meet substantial financial requirements, which might not be possible with personal loans.

No Usage Restrictions: Unlike some loans that have specific end-use requirements, LAP offers the flexibility to use the funds for any purpose.

Improves Credit Score: Timely repayment of a LAP can significantly improve a borrower’s credit score, enhancing their future borrowing capacity.

Disadvantages of Loan Against Property

Risk of Losing Property: The biggest drawback is the risk of losing the property if the borrower defaults on the loan. This makes LAP a significant financial commitment.

Lengthy Processing Time: Due to the property valuation and legal verification processes, the disbursement of LAP can take longer compared to unsecured loans.

Higher Costs in Long Run: Although the EMIs are smaller due to longer tenures, the total interest paid over the loan period can be considerably higher.

Eligibility Criteria: Strict eligibility criteria related to income, property condition, and legal clearances can make it challenging for some borrowers to qualify for LAP.

Eligibility Criteria for Loan Against Property

Age: Generally, borrowers should be between 21 and 65 years of age.

Income: Stable and sufficient income to ensure timely repayment of EMIs is crucial. This includes salary slips, income tax returns, and bank statements.

Property Ownership: The property must be in the borrower’s name and free from any legal disputes or encumbrances.

Credit Score: A good credit score enhances the chances of loan approval and favorable interest rates.

Employment: Both salaried individuals and self-employed professionals/businessmen can apply for LAP. However, the income stability and continuity will be closely scrutinized.

Documentation Required for Loan Against Property

Proof of Identity: Passport, Voter ID, Aadhaar, or any government-issued ID.

Proof of Address: Utility bills, passport, or any document that verifies the current address.

Income Proof: Salary slips, IT returns, bank statements, and proof of business or professional income for self-employed individuals.

Property Documents: Title deeds, sale agreements, property tax receipts, and any other documents related to the property.

Photographs: Recent passport-sized photographs of the applicant.

Loan Against Property vs. Personal Loan

Collateral Requirement: LAP requires property as collateral, while personal loans do not.

Loan Amount: LAP generally offers a higher loan amount compared to personal loans.

Interest Rates: Interest rates for LAP are lower than those for personal loans.

Tenure: LAP offers a longer repayment tenure compared to personal loans, which typically have a tenure of up to 5 years.

Processing Time: Personal loans have faster processing times due to less documentation and no collateral requirement.

Conclusion

A loan against property is a versatile and beneficial financial tool for individuals needing substantial funds at lower interest rates. It leverages the value of a property to provide liquidity without relinquishing ownership. However, the risk of property forfeiture and the longer processing time are significant considerations. Borrowers must carefully assess their financial situation and repayment capability before opting for LAP, ensuring that they can meet the EMI obligations to avoid the risk of losing their valuable asset.

Latest Post

- Tips and Tricks to Get a Personal Loan with a Low CIBIL Score

- How ECLGS Loans Help MSMEs and Large Enterprises Weather Financial Crises

- Comparing MUDRA and ECLGS Loans: Which One is Right for Your Business?

- How to Apply for an ECLGS Loan: Step-by-Step Guide

- The Role of ECLGS in Post-Pandemic Business Recovery in India

- How to Apply for a MUDRA Loan: A Step-by-Step Guide

- Understanding the Impact of MUDRA Loans on Small Businesses in India

- What is an ECLGS Loan?

- What is a MUDRA Loan?

- Difference Between MUDRA and ECLGS Loans

- Why Choose ICICI Lombard

- Benefits of Taking a Business Loan from Godrej Capital

- Benefits of Taking a Business Loan from Aditya Birla Finance

- Benefits of Taking a Business Loan from Tata Capital

- Benefits of Taking a Business Loan from Bajaj Finance

- How to Perform a SWOT Analysis for an Individual in Their Late 30s: A 10-Step Guide

- What is Dropdown OD Overdraft

- How to Create and Sell Digital Products: A Comprehensive Guide

- How to Start a Side Hustle with Minimal Investment

- India’s Leading Electric Car Brands and Their Future Plans for 2025

{"ticker_effect":"slide-h","autoplay":"true","speed":3000,"font_style":"bold"}